Zero-carbon shipping for CCS

Fossil-fueled ships are quietly gutting CCS budgets with EU ETS fees and lost credits, but multi-fuel vessels can bridge the transition into green shipping to remove the losses.

- Dirty ships kill CCS budgets

- Funding the transition

- Market signals

- Conclusion

- Footnotes

- Bibliography

- Backlinks

Originally published as a subscriber article in the Carbon Capture Journal (issue 101), a leading magazine for carbon capture storage and utilisation, and subsequently presented at the Zero Emissions Platform, the official EU advisor on industrial carbon management.

While CCS is essential for decarbonising industry, the ships built to transport captured CO₂ are quietly undermining the economics they’re meant to enable. Under the EU ETS, fossil-fueled carriers incur rising emissions costs that get passed through to emitters, while biogenic producers lose carbon credits for every tonne of CO₂ emitted in transit. As carbon taxes climb toward €100–149/t, building more dirty carriers is a trap that ruins CCS budgets from the inside.

Ammonia-powered ships offer a zero-carbon alternative, and multi-fuel engine designs provide a practical bridge: vessels that run on conventional fuel today and switch to ammonia as bunkering infrastructure matures. The technology is ready; the challenge is commercial. Layered capital structures combining public de-risking, sustainability-linked financing, and long-term charters can close the funding gap, and with 430 ammonia-ready hulls already in the global orderbook, the market is gently moving.

There is something absurd about building ships to transport captured CO₂ that themselves emit CO₂ in the process. Under the EU ETS, this absurdity now has a price tag; one that is quietly gutting CCS 1 budgets and eroding the carbon credits of biogenic emitters. As carbon taxes rise, fossil-fueled CO₂ carriers become a trap: the very ships meant to enable decarbonisation are undermining it.

Ammonia-powered ships, supported by multi-fuel engine designs, offer a practical way out. They are expensive, and the fuel infrastructure does not yet exist at scale. But the commercial and financial risks can be managed through proven capital structures; and the alternative, continuing to build dirty carriers, is worse.

Dirty ships kill CCS budgets

Under the EU ETS, cargo ships above 5,000 gross tonnage 2 must surrender EUAs 3 for 70% of their CO₂ emissions, increasing to 100% from 2026. With EUA prices projected at €100/t by 2027, the numbers get serious quickly. A CO₂ carrier burning MGO 4 on a 550 nautical mile 5 transit from Belgium to the Northern Lights terminal, emitting roughly 0.5 tCO₂/nm, 6 would incur €19,250 in EU ETS costs at the 70% rate. Northern Lights has opted for LNG-fueled ships (0.32 tCO₂/nm) which reduces the cost by about 21% (Istrate2022, pp.76), but even that falls far short of the IMO’s 50% greenhouse gas reduction target by 2050.

These costs matter more in CCS than in most shipping sectors because CO₂ management is more akin to low-margin waste management than the high-margin oil business. Shipping companies pass EU ETS costs through to customers via tonne-mile pricing, 7 and plant managers I’ve spoken with are rightly alarmed. For biogenic emitters the damage is double: CO₂ emitted during transport subtracts from the negated emissions ledger (the net CO₂ removed after accounting for lifecycle emissions) lowering their ability to sell carbon credits and reducing their return on investment on CCS.

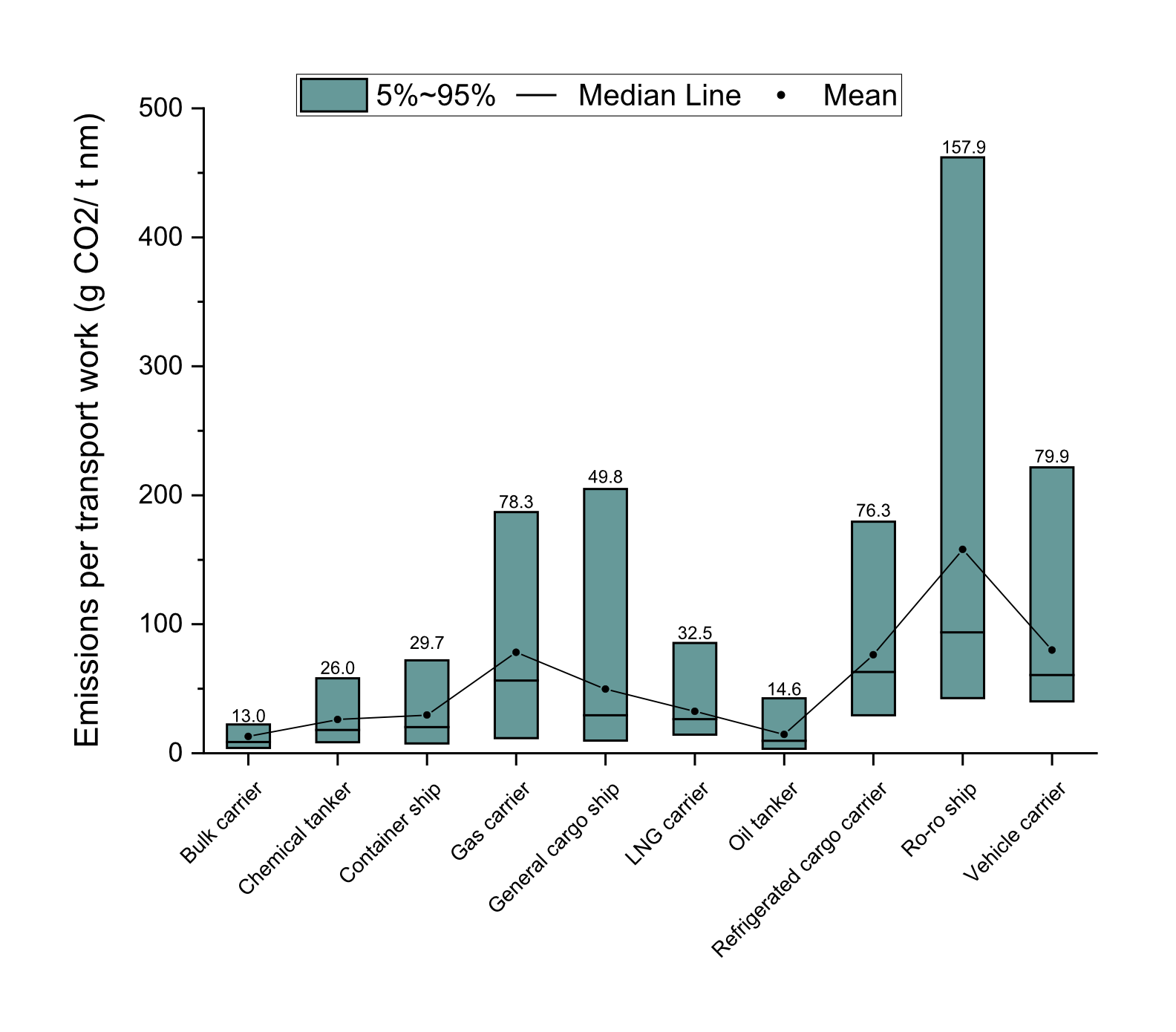

Emissions from fossil-fueled ships also vary widely by vessel category, which matters when calculating the financial strain on CCS projects. Bulk carriers emit around 16.4 g CO₂/t·nm, oil tankers 20 g, chemical tankers 26 g, and ro-ro ships as much as 158 g CO₂/t·nm (Istrate2022). Based on 2019 THETIS-MRV data, less efficient vessels emit nearly ten times more per tonne transported than bulk carriers, amplifying EU ETS costs for operators reliant on MGO or LNG. A CO₂ carrier running on MGO would categorically fall in the mid-range of these figures. An IMO report (Faber2020) underscores that such inefficiencies, coupled with projected emission increases of 90–130% by 2050, make a swift shift to zero-emission fuels like ammonia essential—both to protect CCS budgets and to meet decarbonisation goals more broadly. Bloomberg’s EU ETS price projections of €149 by 2030 would only sharpen the problem.

The outcome is clear: even purpose-built CO₂ carriers running on fossil fuels will drain CCS budgets and halt decarbonisation. The industry needs zero-carbon fuels, and it needs them before the fleet is locked into another generation of dirty ships.

The scale of the challenge

The urgency of cleaning up CO₂ shipping becomes starker when you consider the volumes involved. Global CO₂ emissions from burning fossil fuels reached 40 gigatonnes 8 in 2022. That’s enough to cover Alaska, Texas, and California under eight metres of gas (Tso2023). The EU wants to capture 250 megatonnes a year by 2050, but CCS is only as useful as the transport infrastructure behind it.

Commercial transport and storage value chains are maturing. Northern Lights can currently handle 1.5 megatonnes per year, but its shipping slots are fully booked, leaving emitters stranded. I’ve heard plant managers gasp when they realise the lack of transport options kills their capture projects before they start. Pipelines sound promising but cannot reach everywhere, and their long lead times and high upfront costs make rapid deployment impractical; ships are a necessary piece of the puzzle (Lockwood2025). Yet a typical carrier hauling 10–25 kilotonnes of liquefied CO₂ per trip is barely a dent in 40 gigatonnes, and retrofitting current fleets will not solve the capacity gap either. 9 The global fleet of CO₂ carriers 10 needs to expand dramatically, 11 and the ships being built now will define the emissions profile of CO₂ transport for decades.

That is why the fuel choice for new carriers is not a secondary consideration. It is the decision that determines whether CCS transport scales affordably or becomes a budget sinkhole.

Ammonia and multi-fuel as the bridge

Ammonia is the most scalable zero-carbon fuel suited to long-distance shipping routes. It produces no CO₂ when burned, which means CO₂ captured from emitters can reach storage sites without generating additional emissions along the way; aligning directly with the purpose of CCS.

Ammonia-powered vessel designs are generally considered mature enough for deployment. The challenge is commercial, not technical. Ammonia vessels cost 50–130% more than conventional ships, driven by lower energy density (requiring larger fuel tanks), advanced engine technology (requiring heavy R&D investment), and the safety systems needed to handle a toxic, corrosive fuel (Boyland2022). On top of vessel costs, the global ammonia bunkering network barely exists. These factors create compounding risks for anyone considering an order: market risk from uncertain returns on expensive fuel technology, credit risk from financier caution about long-term viability, infrastructure risk from an incomplete fuelling network, and technology risk from the possibility that newer designs could leapfrog current ones.

With limited capital support, widespread deployment will take time, and that delay creates uncertainty around the practical costs of CO₂ transport for both shipowners and emitters. These logistical uncertainties slow CCS deployment at scale. They can also push the overall cost of CCS to a point where industrial emitters lose their incentive to implement it, despite the significant carbon taxes on their operations.

How, then, can the industry de-risk the transition without waiting for a complete ammonia infrastructure to materialise?

Multi-fuel engines offer the most pragmatic answer. Ships equipped with engines that can run on both conventional fuel and ammonia lower the immediate risk for shipowners: they can operate on existing fuels today and switch to ammonia as the bunkering network matures. This is not a theoretical proposition. The Norwegian shipowner Höegh Autoliners recently took delivery of the first of twelve new ammonia- and methanol-certified pure car and truck carriers. When an industry heavyweight commits to that kind of order, it does more than reduce their own transition risk, it signals to the broader market that the time to invest in ammonia fuel infrastructure is approaching. Multi-fuel ships are a platform for bridging the commercial gap while sustainable fuel infrastructure scales up and costs come down.

Funding the transition

The technology for ammonia-powered vessels exists. What lags behind is the economic framework to support their commercial rollout. Public grants and subsidies (often the lifeblood of critical infrastructure innovation) are still primarily directed at research and development rather than deployment (Boyland2022).

Achieving commercial viability requires institutional investors to step in alongside public capital, because deep-sea shipping is integral to the global economy and the sums involved exceed what any single shipowner or government programme can cover. The Nordic Green Ammonia Powered Ships (NoGAPS) project has proposed a framework built around four levers that, taken together, can reduce the financial burden on shipowners while lowering risk for institutional investors (Boyland2022).

The first lever is cost-efficient, dual-fuel vessel design; precisely the multi-fuel approach discussed above. Dual-fuel engines allow vessels to switch between conventional and ammonia fuels, which minimises both capital and operational costs during the transition while mitigating residual value risk. A ship that can burn multiple fuels is less likely to become a stranded asset if market conditions shift.

The second is competitive financing. Sustainability-linked loans, where interest rates decrease if environmental targets are met, can make ammonia-powered vessels more attractive to banks that would otherwise price in the technology risk. Combining these with traditional bank lending creates a layered financing structure that reflects the genuine risk profile rather than applying blanket premiums.

The third lever is public sector de-risking. Government capex grants and export credit agency guarantees directly reduce the financial burden on shipowners, bridging the gap between what the market will fund today and what the transition actually costs. Without this, the first movers bear disproportionate risk, which slows the entire fleet transition.

The fourth is premium long-term charter agreements. Securing contracts with reputable charterers provides stable revenue streams that reduce credit and residual value risk for lenders and investors. For a shipowner taking the leap on ammonia, a ten-year charter with a creditworthy counterparty is the difference between a fundable project and a speculative bet.

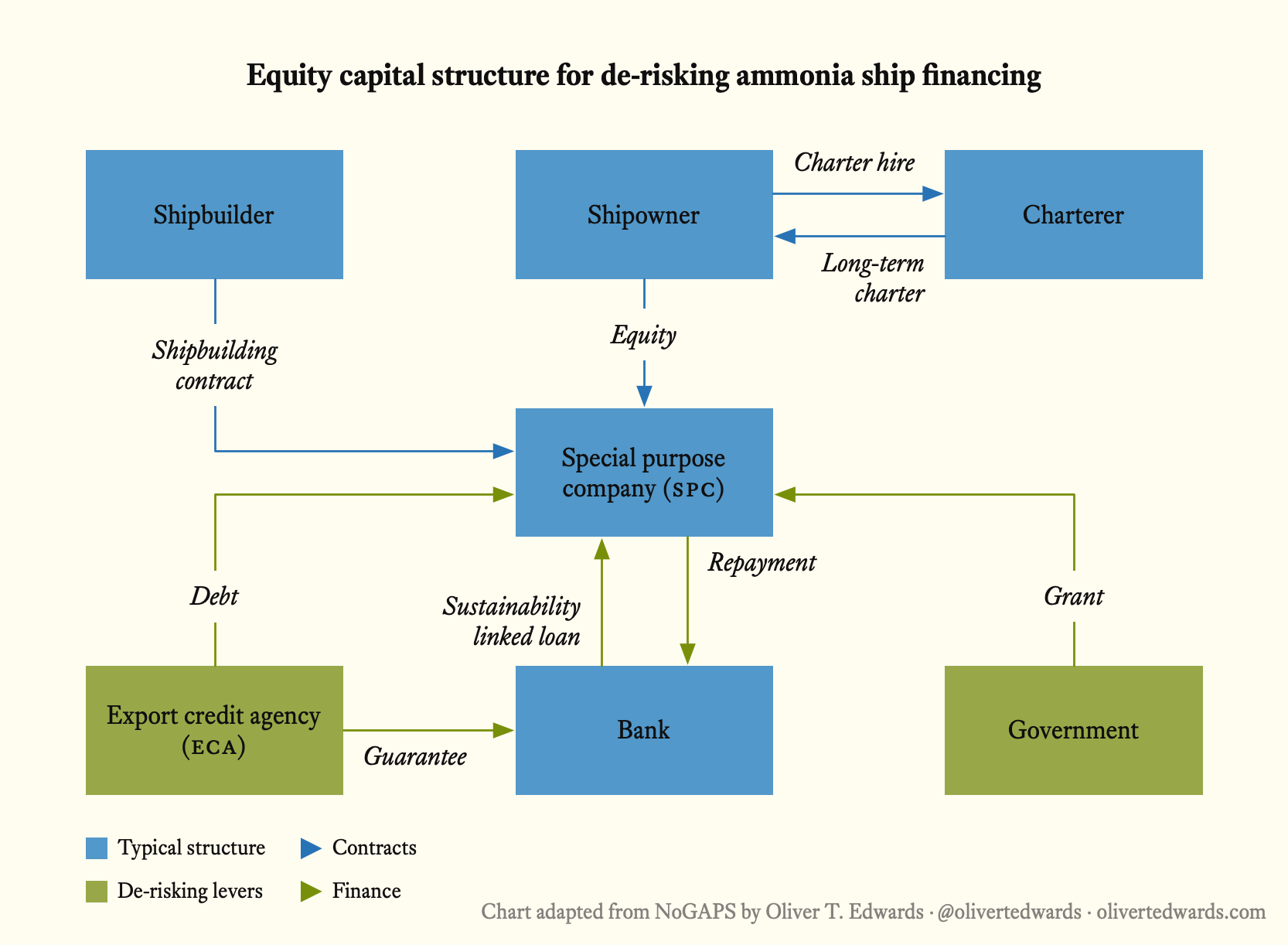

Equity model

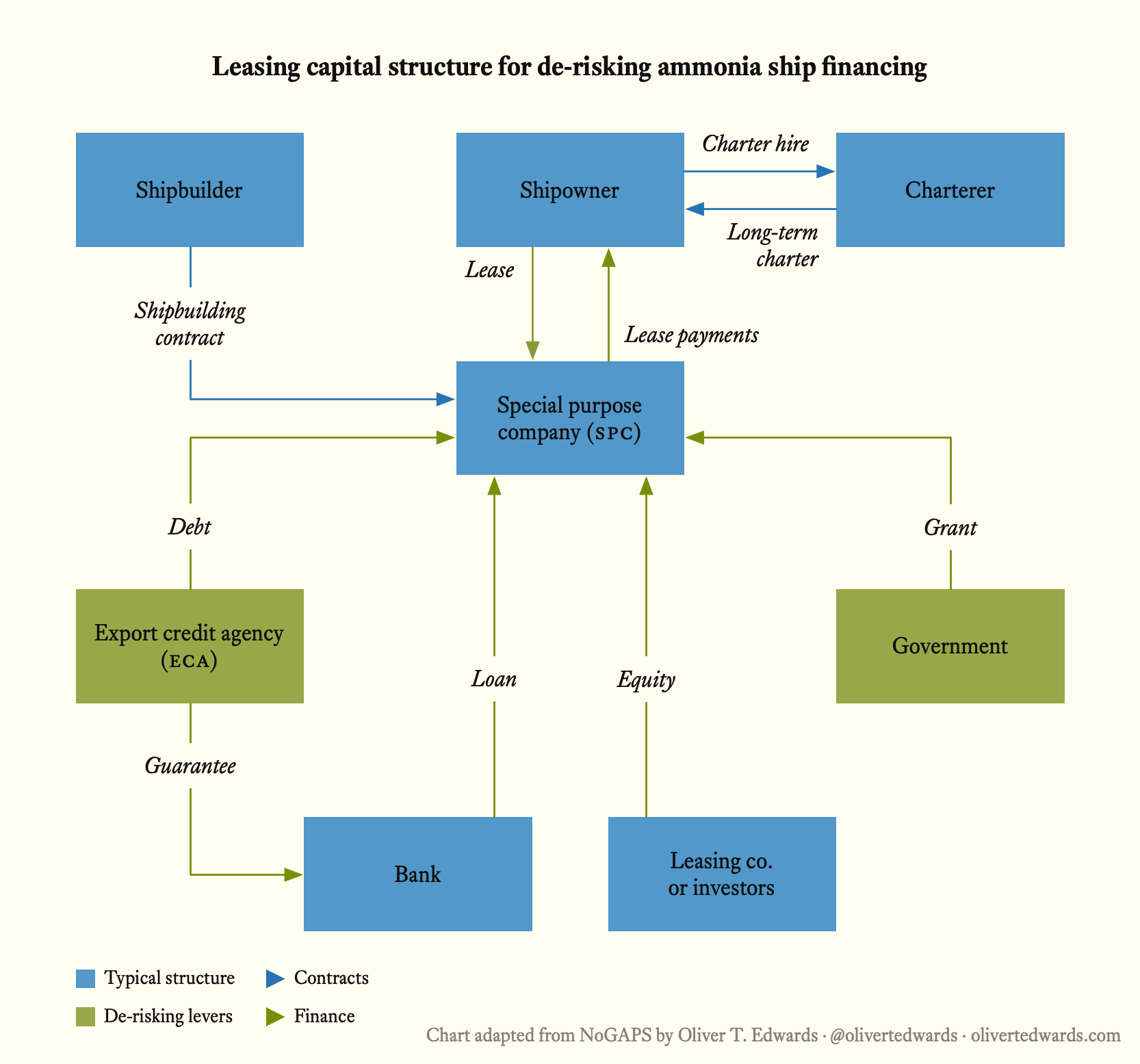

In the equity structure proposed by NoGAPS, the ship is owned by a special purpose company (SPC) created solely for owning and operating the vessel. The shipowner provides a significant portion of the equity, which anchors the financing and signals commitment to lenders. A bank then offers a sustainability-linked loan to the SPC, tied to specific environmental targets that can improve terms over time. A government grant helps offset the premium cost of building an ammonia-powered ship compared to a conventional vessel, while a debt or loan guarantee from an export credit agency reduces the bank’s exposure and secures more favourable lending terms. The shipowner also secures a long-term charter agreement to provide the stable revenue needed to service the debt, though the higher operating costs of ammonia ships can make negotiating these charters more difficult.

This structure works when the shipowner has sufficient capital and creditworthiness to anchor the deal. But not every operator does, which is where the leasing model comes in.

Leasing model

The leasing structure is designed to reduce the upfront capital requirement for the shipowner by spreading ownership risk across a group of investors or leasing companies. Instead of the shipowner providing the anchor equity, a consortium of investors funds the SPC, with the shipowner contributing a smaller share. A bank loan complements the equity, and the same government grants and ECA guarantees apply. The ship operator then enters a leasing agreement with the SPC (using the vessel without the full capital commitment of ownership) while also securing a long-term charter agreement with a charterer to stabilise cash flow.

The leasing model is particularly attractive for operators who are cautious about the financial risks of new technology. It lowers the barrier to entry by allowing participation in the ammonia transition without betting the company on it, while still providing investors with the stable returns they need to commit capital.

Both structures depend on all four levers working in concert. Remove any one (the public grants, the long-term charters, the sustainability-linked financing, or the multi-fuel design itself) and the risk profile shifts enough to stop deployment. The lesson from other infrastructure transitions is that this kind of layered de-risking is how capital moves into new technology. Waiting for costs to fall on their own is not a strategy; it is how you end up with a fleet of dirty ships locked in for thirty years.

Market signals

The maritime sector’s move toward ammonia is no longer hypothetical. As of late 2024, Clarksons reported a combined ammonia-ready fleet and orderbook of about 430 ships, and the Viking Energy was slated to become the world’s first ammonia-powered offshore support vessel by 2026.

The regulatory tailwinds are strengthening too. The inclusion of shipping under the EU ETS as of 2025, alongside the FuelEU Maritime regulation’s push for lower greenhouse gas intensity in ship fuels, creates a tightening cost environment for fossil-fueled operators. These regulations will accelerate ammonia adoption while building out infrastructure that also supports CO₂ transport and storage; stabilising or reducing transport costs for CCS and encouraging long-term carbon management projects through more predictable cost structures.

Conclusion

Scaling CCS to handle gigatonnes of annual CO₂ emissions is already a brutal logistics challenge. Compounding it with the EU ETS costs of fossil-fueled carriers (and the erosion of biogenic carbon credits) is like a self-inflicted wound. Multi-fuel ships like Höegh Autoliners’ ammonia-ready carriers offer a bridge, and 430 ammonia-ready hulls in the global orderbook suggest the market is beginning to move.

But deployment risks and funding gaps remain real. The capital structures outlined here (equity and leasing models layered with public de-risking, sustainability-linked financing, and long-term charters) provide a more or less proven path. Institutional investors need to get onboard, because if maritime transport becomes a bottleneck for CCS, the cost will be measured in megatonnes of CO₂ that never reach storage.

-

Carbon capture and storage (CCS) is a process by which carbon dioxide (CO2) from industrial installations is separated before it is released into the atmosphere, then transported to a long-term storage location. ↩︎

-

Gross tonnage (GT) is a measure of a ship’s overall internal volume, used to determine the size of a vessel for regulatory and commercial purposes. Under the EU ETS, the obligation to surrender EUAs for CO2 emissions applies to cargo and passenger ships with a gross tonnage above 5,000, targeting larger vessels with a significant environmental impact due to their size and fuel consumption. ↩︎

-

EU Allowances (EUAs) represent an allowance to emit 1 tonne of CO₂ each, and they are traded as futures on platforms like the European Energy Exchange (EEX). In practice, for maritime operators, the cost of purchasing EUAs to cover emissions under the EU ETS can function like a pre-purchased tax on CO₂ emissions. ↩︎

-

Marine gasoil (MGO) and heavy fuel oil (HFO) are two common marine fuels with different compositions, properties, and applications. HFO is a residual fuel, meaning it’s the heavier byproduct of crude oil distillation after lighter fractions like MGO have been removed. MGO, on the other hand, is a distillate fuel, meaning it’s a lighter, more refined fraction of crude oil. ↩︎

-

Nautical miles; 1 nautical mile (nm) is 1.852 kilometers (km). ↩︎

-

MGO as a tanker fuel generally seems to emit around 0.5 tonnes of CO₂ per nautical mile supported by Istrate (2022), and our internally acquired research at Normod Carbon. ↩︎

-

Tonne-mile price; the cost charged by shipping companies per tonne of cargo transported per nautical mile, reflecting operational and regulatory expenses like EU ETS costs. ↩︎

-

Metric tonnes; 1 gigatonne (Gt) is 1,000,000,000 tonnes, 1 megatonne (Mt) is 1,000,000 tonnes, and 1 kilotonne (Kt) is 1,000 tonnes. Though fairly comparable, a metric ton is 2,204.6 lbs, which is a little more than the American ton’s 2,000 lbs and a little less than the British ton’s 2,240 lbs. ↩︎

-

Rough guestimate; the global LNG tanker fleet consisted of 772 ships in 2023, including FSRUs. Assuming each ship has a carrying capacity of 10–25 kilotonnes of CO2 the fleet could theoretically hold between 7,720 and 19,300 kilotonnes. In this case, LNG carriers would need retrofitted for CO2 transport since LNG has different density, storage, and operational contraints. ↩︎

-

The global fleet of CO₂ carriers in commercial operation is three as of December the 4th, 2025. ↩︎

-

A typical carrier can haul 10-25 kilotonnes of liquefied CO₂ per trip, barely a dent in 40 gigatonnes, so retrofitting old vessels won’t solve capacity needs. ↩︎

Bibliography

-

Tso2023 “How much is a ton of carbon dioxide?”, MIT Office of Sustainability

MIT explainer providing physical intuition for the scale of CO₂ emissions — a single metric tonne occupies a 27-foot cube; a typical American generates 15 tonnes annually; steel manufacturing produces nearly 2 tonnes of CO₂ per tonne of steel. The piece is most useful as a reference for communicating the physical scale of the decarbonisation challenge to non-specialist audiences: numbers like 40 billion tonnes of global annual emissions require grounding before they carry any meaning, and Tso’s framework provides that grounding concisely. Electric vehicles, for context, reduce per-kilometre emissions to roughly 22% of a combustion equivalent — but only when charged on a genuinely low-carbon grid.

-

Lockwood2025 “Building Future-Proof CO₂ Transport Infrastructure in Europe”, Clean Air Task Force

Clean Air Task Force analysis of the CO₂ transport infrastructure required to meet the EU’s 2050 net-zero target and the 250 Mtpa storage ambition set out in the Industrial Carbon Management Strategy. The paper calculates that Europe needs 15,000–19,000 km of CO₂ pipelines by 2050, supplemented by ships, rail, and road for emitters that pipelines cannot reach affordably — a combination that mirrors the multi-modal architecture the LNG industry eventually converged on. The analysis makes the case for a cohesive EU regulatory framework governing access, pricing, and cross-border coordination, noting that the current patchwork of national initiatives risks replicating exactly the fragmentation problem that shared infrastructure is meant to solve.

-

Istrate2022 “Quantifying emissions in the European maritime sector (EUR 31050 EN)”, Publications Office of the European Union

JRC analysis quantifying greenhouse gas and air pollutant emissions from ships transiting EU ports in 2019, drawing on the MRV-THETIS database, alongside a meta-analysis of life cycle assessments for maritime fuel alternatives. The emissions picture is clear: shipping is a significant and growing source of CO₂, SO₂, NOₓ, and particulate matter, and energy efficiency improvements alone are insufficient to bend the trajectory without fuel switching. The LCA meta-analysis documents the extent to which the decarbonisation potential of alternative fuels depends on the upstream energy chain — green ammonia and green hydrogen perform well only when the electricity used to produce them is genuinely low-carbon, a condition that constrains deployment timelines considerably.

-

Faber2020 “Fourth IMO GHG Study 2020”, International Maritime Organization

The study documents a 9.6% rise in total shipping greenhouse gas emissions between 2012 and 2018, reaching 1,076 million tonnes CO₂e, with international shipping maintaining a stable share of roughly 2% of global CO₂ emissions throughout. Carbon intensity improved by 21–29% vessel-based over the same decade, but the efficiency gains are being outpaced by growth in trade volumes; a decoupling problem that has not improved since. Under the study’s central scenarios, shipping emissions in 2050 could reach 90–130% of 2008 levels, making the sector’s decarbonisation trajectory one of the more difficult to align with 1.5°C without structural shifts in fuel and propulsion technology.

-

Boyland2022 “NoGAPS: Nordic Green Ammonia Powered Ships: Phase 2: Commercialising Early Ammonia-Powered Vessels”, Nordic Innovation

The NoGAPS project assembled Nordic shipping and energy players to develop the M/S NoGAPS, a first-of-a-kind ammonia-powered gas carrier, and this final report documents what commercialising it actually required: design trade-offs, propulsion architecture, and financing strategies for a vessel type the market had never seen. The core challenge is identical to the one facing CO₂ shipping and every other alternative-fuel pioneer; zero-emission vessels cannot be made economic in isolation when the bunkering networks, fuel pricing frameworks, and regulatory infrastructure that would justify their unit costs have not yet been built.